The problem arises when people don’t pause to think about what the credit card is to them.

What is a credit card?

This is easy; it’s that rectangular bit of plastic that you use instead of cash. Well that’s deceptively simple and unfortunately is about as much thought that most people put into credit cards and why they are a financial trap for so many.

Well yes, it is still mainly a bit of plastic, but it doesn’t have to be when it is loaded into your digital wallet. It already is for many, and will increasingly become the norm, as standard functionality on your phone or watch or embedded chip or tattoo. I wonder if we will be still calling them credit cards when nobody is still carrying the bit of plastic?

Musings aside, credit cards are three things:

- Access to credit – you can spend when you don’t have money.

- A payment mechanism – convenience of being able to complete transactions remotely or when you just don’t want to carry cash.

- A rewards bonus for spending

The problem arises because people don’t pause to think about what the credit card is to them.

Labelling of credit cards has added to the confusion

In Australia, the banks built the first credit cards 40 years ago through a proprietary system they jointly owned, Bankcard. It had no overseas capability being a domestic system. Now the card systems are owned by Visa and Mastercard and the banks issue cards on one system or the other. American Express issues its own cards on their own system. (I’ll deal with various roles later).

The banks developed:

- Basic cards

- Silver cards

- Gold cards

- Platinum cards

- Black cards

- Etc.

And that’s when the problems started.

You still see those labels around, and they mean that you get more benefits – rewards, travel insurance, concierge services – as you move towards platinum. And here’s the rub, you also pay a higher interest rate and higher annual fee.

Over the years Black has been introduced and all sorts of branding flattery to make us feel successful and better about ourselves, but there are essentially only two types of cards, and if you get this clear you won’t make the mistake

- Low rate (and low fee) cards – designed to provide the credit function of credit and the payment functions

- Rewards cards (plus premium functions) – designed to give add-on benefits to people using cards as a payment mechanism

My pet hate; people getting into the wrong sort of card.

CREDIT CARDS AND DEBT

How you get credit through your credit card

There are three ways that you use a credit card for credit

- Instead of a bank loan. Years ago, when you needed cash as a consumer for any purpose aside from housing, you took out a personal loan. The banks then decided it was easier to just give customers a credit card and now the smaller loans are done that way.

- Cash advance. You take your card to the bank or ATM and withdraw cash that you don’t have.

- You don’t pay off the card in full each month. The balance builds up and you end up owing the bank a lot of money.

The last is the worst. You are taking on a liability without thinking about it, by accident. You have made yourself a victim of debt by stealth. The problem is not the credit card, it is your spending problem. If the credit card means that you can’t say no to spending, cut up your card, work out a programme to pay back the debt and get a debit card for transaction convenience.

What about cash advances? Only take them when you know you can repay them in two or three months. If the answer is no, consider whether you need to spend.

As a loan, there can be worthwhile reasons, providing you are not burying yourself in debt you can’t afford to repay and putting yourself behind financially. But you must stick to your repayment plan.

But is the credit card a suitable credit mechanism

Interest rates first

- The average credit card interest rate is around 14%.

- The average personal loan rate is 10% / 11%.

- But then there are 20 credit cards with rates below 10%.

So in terms of rates, there are cards that are fine compared to alternative credit sources.

But there is another problem. Credit should always come with a repayment solution. Personal loans require you to make your monthly repayments, which help you to get the debt behind you. Credit cards come without the discipline of fixed repayments and require only that you repay 2% to 3% of the outstanding balance each month. If that is all you pay, it can take you 10 years to repay a $2,000 debt on your average credit card. But it is too easy to do the minimum rather than sticking to your plan.

For most people repaying is easier than saving because the repayment is a discipline, and it is harder to self-impose that discipline than have it set by the lender. So, not an ideal credit mechanism.

What if you are already in debt on your card?

In essence credit card debt is bad debt. Because it was incurred for a relatively small current expenditure or an accumulation of expenditures, you are not taking on a debt to improve your long term financial wellbeing. To the contrary, you are harming you finances by paying the bank interest that could otherwise go towards savings.

What this means is that any debt on your credit card should be cleared in the short term. If this is how you treat credit card, you are on the right track. Ultimately, you should have no debt on your credit card. Zero.

But we know this is not the case. The level of credit card debt in Australia is in decline, but it is still a whopping $32 billion.

If part of this is you, get it repaid ASAP. No, sooner.

The three step plan to get you out of credit card debt

- So, if you have your share of the $32 billion, set in place a repayment plan and stick to it. Set up the direct debit from your salary account to your credit card for every pay day. You never have the money, so it is never yours.

- To make it easier, get into a low rate card. There is a range of cards with rates below 10%, but a much bigger range above 20%. A 20% rate eats a lot out of your repayments that is not going towards paying off your debt.

- Most importantly stop spending.

Balance transfer, a way out of debt or a debt trap?

A balance transfer deal gives you a very low rate for an introductory period on the balance you have on another card and transfer to your new card. These days, usually 0% and 12 months. They can come with fees, so make sure these are not too high.

The principle is that you use the 12 months to pay off the debt and if you stick to your repayment programme, they’re a great deal.

But that’s not typically what happens. What usually happens is that the cardholder doesn’t have the discipline to keep the repayments up every month, then makes purchases on the card that add to the balance, leaving a still large debt on the card which now becomes a high rate card.

Banks make money by charging interest on loans, so when you see zero interest on a credit product you have to wonder. This is how it works.

The answer is simple. Make a repayment that will clear the loan in the 12 months and put the card in the bottom draw locked away until you have cleared the debt.

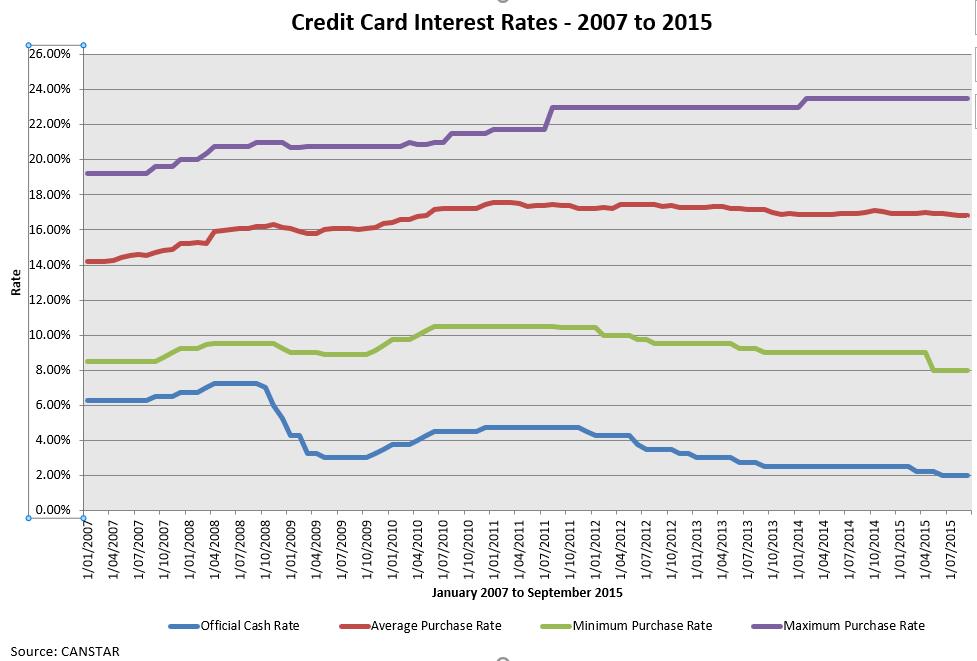

Interest rate moves compared to cash rate

Banks love credit cards and credit card debt in particular.

The chart below shows the movement of credit card interest rates compared to the RBA cash rate post GFC. As the cash rate has been falling, from 7.5% to 1.5%, credit card rates at the top end have been rising, by round 4%. Even the average credit card rate has gone up by round 1%. The margin over cash rate has risen from 8.5% to 13%!

Yes, the banks have higher rates of bad debts on cards, but not that much higher. What is there not to love!

CREDIT CARDS AND TRANSACTIONS

Transactions in the old days BCC

In the bad old days there was just cash and cheques. Cash came from the teller at the bank and cheques were the convenient form of transaction as they didn’t require an expedition to the bank, but not all businesses accepted them.

Then came credit cards (they pre-dated the ATM) and a whole new world of convenience opened up. Most of our retail purchases (even online we link our paypal to our credit card) are still made through credit card and they still work basically as they did from the outset.

We make our purchases through the card, receive a monthly statement aggregating our month’s spending to a single payment, and make at least the minimum payment by due date.

At point of sale it looks a little different. From a click clack machine (credit card imprinter) that embossed the card number on three carbon copies that were then handwritten with the transaction, to a card inserted with PIN, to contactless, then digital wallet …… to chip embedded above the left eye? But the essence of the transaction is the same.

There is a substitute if credit cards are a health hazard

For those who find the plastic to be an overwhelming spending temptation, it doesn’t mean a return to cash. The debit card allows the same transactions, but unbundles the credit function from the card, so that you make the transaction direct to a deposit account that holds money you own. You won’t earn reward points, but if control of your spending is your problem, rewards were never part of the solution. You’re spending your own money which will keep you out of trouble.

CREDIT CARDS FOR REWARDS AND BENEFITS

What are credit card rewards?

On some credit cards, you earn rewards point on the dollar spend put through the card. The more you spend the more points and rewards benefits you receive.

The rewards can take multiple forms:

- Flight rewards – most commonly with the points transferred to Qantas or Virgin

- Cash – with dollars credited to your credit card

- Shopping coupons – for spending at supermarkets, department stores, specialty retailers

- Merchandise – toasters, etc selected from a catalogue

A more recent addition has been an annual domestic flight awarded irrespective of spend and in addition to other rewards.

Rewards are worth the effort but not always

Rewards should be treated with care. They can be a real benefit but should not be chased.

If you don’t manage to repay your credit card in full every month, forget rewards. The annual fee and interest rate are generally higher and you should be taking a low rate, low fee card.

Watch the annual fee when you choose a rewards card. If you are only spending $2,000 a month, the better rewards programme will not compensate for a high annual fee card.

If there is a higher surcharge (the fee the merchant sometimes charges the customer for using the card) on one of your cards, use the cheaper one irrespective of the rewards. Higher rewards will rarely compensate for a surcharge.

Do not increase spending to earn higher rewards. The rewards return will not be high enough to compensate you for interest paid or lost.

The key when it comes to rewards is to choose the right card, and then ignore the rewards and treat them as a nice little bonus when you get something back out of the programme.

Which sort of reward should you choose?

The two things to consider are return on your spend – the dollar value of the rewards you earn for what you spend on the card – and what form you prefer to take your rewards.

Flight rewards – Typically deliver the highest return. Better suited to higher spend levels – at annual card spend below $30,000 it takes too long to earn a flight.

Cash – Obviously the most versatile and flexible reward, but the return is the lowest of all categories.

Shopping vouchers – Near to cash when redeemable at a supermarket for the essentials of life. More a luxury when redeemable only at a high end department store. Select the programme compatible with where you like to shop. Reasonable return and suits smaller spends as well.

Merchandise – Deliver a reasonable return, but limited to the catalogue merchandise (how many toasters do you need!).

Which card should you then choose?

More than anything else, this is about the rewards return – the dollar value of rewards earned for the dollars you spend minus the annual fee. More is better.

THE INDUSTRY

How stakeholders work together and get paid

| Consumer | Issuing Bank | Acquiring Bank | Scheme Provider | Retailer | |

| Role | The cardholder and initiator of the transaction. | The bank that gives you the card. Approves credit limit and takes credit risk. Provides rewards. | The retailer’s bank that provides the hardware and takes transaction risk. | Visa / Mastercard provide the infrastructure & processing. | Accepts card payments. |

| Interchange of fees and charges | Pays interest and annual fee to issuing bank. May pay surcharge to retailer. | Charges interest and fees. Collects interchange fee from issuing bank. | Charges retailer a card services fee, which is shared with issuing bank. Pays scheme provider. | Charges the acquiring bank for the transaction | Pays acquiring bank at a rate based on volume. May charge consumer surcharge. |

| Revenue | Interest Annual fees Interchange | Card services fee | Transaction charges Platform charges | Surcharge | |

| Expense | Interest Annual fee Surcharge | Credit lossesRewardsProduct overheads | Visa / Mastercard Interchange | Overheads | Card services fee |

| American Express(special case *) | Pays interest and annual fee to Amex. May pay surcharge to retailer. | American Express | American Express | American Express | Pays Amex based on volume. May charge consumer surcharge. |

* American Express is a special case as it stands in place of the issuing bank, the acquiring bank and the platform provider. It is a non-bank and outside the reach of the regulator for credit cards, the Reserve Bank of Australia.

What this explains is that there are three businesses clipping the ticket on your credit card – the bank that issued you the card, the bank that provided the card processing machine to the retailer and the Visa / Mastercard. The last two are essentially business to business between the retailer, the banks and Visa / Mastercard.

Issuers of credit cards

There are various card issuers – banks, credit unions and building societies, and American Express.

The big four, other large banks and American Express issue a range of cards, low rate, low fee and rewards cards. Their lowest rates tend to be higher than the small issuers, but they have moved down since the RBA’s latest interchange regulations.

The customer owned banks, credit unions and building societies generally issue low rate cards, though some also offer rewards cards. The lowest rate cards are issued by these institutions.

As with other parts of the banking market, the Big 4 dominate the market via their incumbency and distribution.

How the issuing bank makes money

The issuing bank has the B2C relationship with you the card user, and it earns revenue from two sources – interchange fees, and fees and interest.

Interchange fees are calculated as a percentage of dollar spend. This means that the highest revenues come from big spending customers. Rewards are offered to attract high spenders and to encourage spending.

Interest rates range from 6.64% to 24.99%, the higher rates usually attaching to high end rewards cards. The highest interest revenues come from customers who leave high debt on their card and are in a high rate card.

In combination, the most profit is earned from customers who spend big, leave debt on their card long term and are in the wrong card. You can see how conflicted the banks are, when it comes to putting people into the right card.

Surcharge and interchange – a thorny issue

The Reserve Bank regulates surcharge and interchange fees and recently introduced a new set of rules, putting a cap on the surcharge retailers can charge their customers and the level of interchange passed from acquiring banks to issuing banks. The regulation is aimed at reducing the cost to consumers and there have been multiple attempts at getting this right.

The latest attempt brought in the toughest regime to date, limiting interchange to a maximum 0.6% on every card in the bank’s portfolio. It resulted to an upheaval in card design.

Returning to the table above, if you reduce revenues via interchange fees, the banks have to reduce expenses somehow. Interest rates are already high, leaving rewards as the cost that had to be cut. The banks cut back earn rates and put in caps on points earned each month.

The complication that arises is that American Express is not subject to the Reserve Bank controls and has not had to restrict fees or rewards.

It has meant that the companion card arrangements that the banks have had with American Express (they issue a Visa or Mastercard with an Amex card) have been unwound. Some banks are now issuing standalone American cards to get around this, but the issue is that Amex is in a position to offer higher rewards than the banks.

Controversies

- Surcharge, merchant fees and interchange – leading to excessive charges to consumers and merchants

- High credit card rates that don’t reduce as other market rates fall

- Credit cards are the biggest debt trap

- Responsible lending has gone out the door

- Limit increases are still being used as a lure

- People in the wrong card – the banks are hopelessly conflicted